Collapse of Cannabis Stocks: A Cruel Reminder of Empty Promises

The cannabis market—hailed as an indomitable contender only a few years ago—has become a dismal wasteland of underperformance and shattered dreams. Tilray Brands, once a poster child for cannabis investments, fell from a staggering $145 per share in 2018 to a humiliating worth of under a dollar. Was it overconfidence, flawed strategy, or the industry’s chaotic legal stalemate that spelled doom? The merciless market has certainly stripped away weaker players, leaving investors grappling with regret.

AdvisorShares Pure US Cannabis ETF (MJUS) tells an equally grim tale. From a peak of $50 per share in early 2021, now clinging to a meager $2.68, this ETF exposes the sector’s glaring failures. What was promised as a vibrant explosion of opportunity has dissipated into unfulfilled regulatory changes and unconvincing business models. So, who remains standing amidst the wreckage?

Turning Point Brands: Diversification or a Smokescreen?

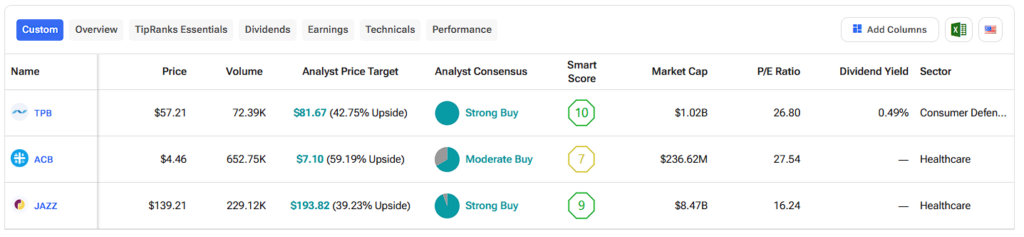

Turning Point Brands has managed to secure itself as an anomaly in the dismal cannabis industry. Doubling in value over the past year, the company—a seller of iconic Zig-Zag rolling papers—appears to understand the importance of diversification. Adding nicotine pouches under its FRE brand and launching a controversial joint venture with Tucker Carlson Media, Turning Point has strategically extended its empire.

Still, one can’t ignore the perception that this “success” hinges on opportunism more than mastery of the cannabis sector. Critics might call it a company profiting from outdated associations rather than groundbreaking innovation in cannabis products. Its entry into the nicotine pouch market, while shrewd, feels like a hedge against the floundering cannabis sector.

Aurora Cannabis: A Fragile Survivor With Scarred Potential

When Aurora soared to a mountain top of $150 per share in 2021, investors dreamed of endless gains. Today, that dream lies shattered as the stock’s value plummeted by a gut-wrenching 95% within five years. Yet, Aurora sees a glimmer of hope. The pivot from Canada’s recreational market into the high-margin international medical cannabis domain may be its saving grace.

Recent earnings reports hint at progress, with adjusted EBITDA hitting a record $7 million. International revenue surged by 93%, overtaking Canadian sales. While the turnaround may look promising, skeptics have every right to question its sustainability. Has Aurora truly redefined itself, or is it another fragile entity desperately clinging to survival?

Jazz Pharmaceuticals: A Diversified Biotech Playing with Fire

Jazz Pharmaceuticals, a name barely associated with cannabis, offers exposure through its acquisition of GW Pharmaceuticals. Epidiolex, a CBD-based drug targeting epilepsy, has become a billion-dollar blockbuster. Jazz’s diversified portfolio—a blend of oncology and sleep-disorder medications—provides stability absent in pure cannabis players.

But while its cannabis-linked efforts seem promising, its role in the sector underscores a lingering dilemma: Can fragmented biotech entities outperform cannabis-focused giants within their own domain? Slim profit margins and dependency on Epidiolex cast shadows over Jazz’s broader cannabis ambitions.

An Industry Limping Toward Redemption

If there’s one takeaway from the carnage of cannabis stock failures, it’s that the industry remains hauntingly volatile. The strongest contenders—Turning Point, Aurora, and Jazz—offer glimmers of hope, but with immense uncertainty threading through their money trails. Investors eyeing this market must contend with a blinding paradox: the alluring potential of cannabis against its ruthlessly volatile reality.

What’s clear is that the cannabis boom wasn’t the financial utopia it claimed to be. The survivors, albeit few, hold onto fleeting optimism, hoping their calculated pivots will rewrite a disastrous history. Only time will reveal whether their moves are born of brilliance or desperation.

Source: finance.yahoo.com/news/tpb-acb-jazz-three-pot-200905362.html

{kind=link}