Overview of Deckers Outdoor’s Troubling Year

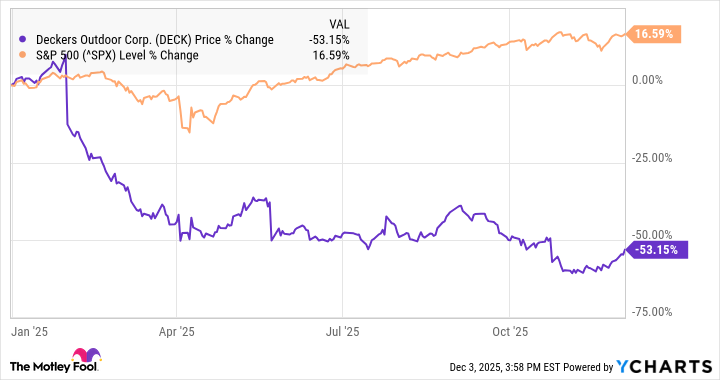

Labeling 2025 as a dismal year for Deckers Outdoor (NYSE: DECK) is an understatement of the highest order. Once soaring high as the parent company of popular footwear brands Hoka and UGG, Deckers has seen its stock price plummet more than 50%—rendering it one of the most regrettable investments within the S&P 500 index. Early year guidance fizzled into disappointment, while external factors like tariff pressures and reduced consumer spending cast ominous shadows over the brand’s financial health.

Declining Sales Amidst Economic Challenges

Deckers’ woes largely stem from a problematic macroeconomic environment, with faltering consumer discretionary spending weighing heavily on its shoulders. Competitors such as Lululemon and Nike have felt similar strains, as well as notable retailers like Chipotle and Target, revealing a broader issue affecting multiple sectors. Specifically, revenue growth for Deckers decelerated to 9% in its fiscal second quarter, with domestic sales crawling to a meager 1.7% increase. Conversely, international sales surged by an impressive 29.3%, which now constitute over 40% of the company’s revenue—strong growth in China underscored this trend. Nevertheless, if domestic sales continue to languish, a robust recovery seems implausible.

Expanding Horizons: Focus on Global Markets

Although investors undoubtedly prioritize domestic results, Deckers’ performance in international markets plays a pivotal role in crafting its long-term success narrative. Citing improvements in regions like China and EMEA (Europe, Middle East, and Africa), the company revealed the opening of its inaugural store in Germany, indicating there’s still ample room for growth. Hoka, in particular, is gaining traction in key European markets, successfully increasing its market share through direct-to-consumer channels.

Examining Margin Resilience

Historically, Deckers is lauded for its ability to maintain strong gross margins, a testament to the power and quality of its brands. Even amidst lackluster performance in the second quarter, the gross margin experienced a slight bump from 55.9% to 56.2%, suggesting that the company isn’t relying on price markdowns to clear inventory. Investors should vigilantly observe gross margins in 2026 to gauge how well Deckers navigates consumer demand fluctuations in the U.S. Maintaining robust margins during challenging times will signal resilience and effective management.

Valuation: A Teetering Stock with Purchase Potential

Investors should heed Deckers’ current valuation, notably impacted after a drastic price fall in 2025, with the stock trading at a modest price-to-earnings ratio of merely 14. This decline suggests a significant portion of the weakness has been incorporated into the stock price. If Deckers manages to stabilize its business and deliver consistent growth, this level could represent a lucrative entry point for investors. Conversely, further dips in valuation might present an even more appealing opportunity for long-term investment.

The Question of Investment in Deckers Outdoor

Before diving into a stock purchase, it’s vital for potential investors to consider that Deckers Outdoor does not appear in the latest list of ten recommended stocks by the Motley Fool Stock Advisor analysts. This gravitation toward other investment opportunities—potentially more promising ones—raises a red flag for immediate investment in Deckers. Nonetheless, the stock has historically shown promise and could still be a viable option if stability returns to its business model amidst expected challenges in 2026.

In sum, as enthusiasts for the long game approach their portfolios, they must weigh both the current adversity and the possible adaptive strengths of Deckers Outdoor in a volatile market.

Source: finance.yahoo.com/news/4-things-watch-deck-stock-172600096.html

{kind=link}