A Shocking Opportunity: Why Progressive Stock Is a Bargain Right Now

The stock market is on fire in 2025, with the S&P 500 soaring by 15% and the tech-heavy Nasdaq Composite even higher at 20%. Yet, amidst this resounding bull market, concerns over absurdly high valuations are causing some investors to panic. Enter Progressive (NYSE: PGR), the renowned auto insurer that’s now trading at a staggering discount—over 30% down from its all-time peak. This presents a glaring opportunity for those with the insight to buy in at such low levels.

Progressive is a dominant player in the insurance sector, boasting a robust 15% market share, making it the second-largest auto insurer behind State Farm. With insurance being a non-negotiable for drivers—backed by regulations mandating coverage—this creates a consistent demand for their products. Progressive’s excellence shines through its superior underwriting practices, where technology, particularly telematics, allows for keen risk assessment and precise policy pricing.

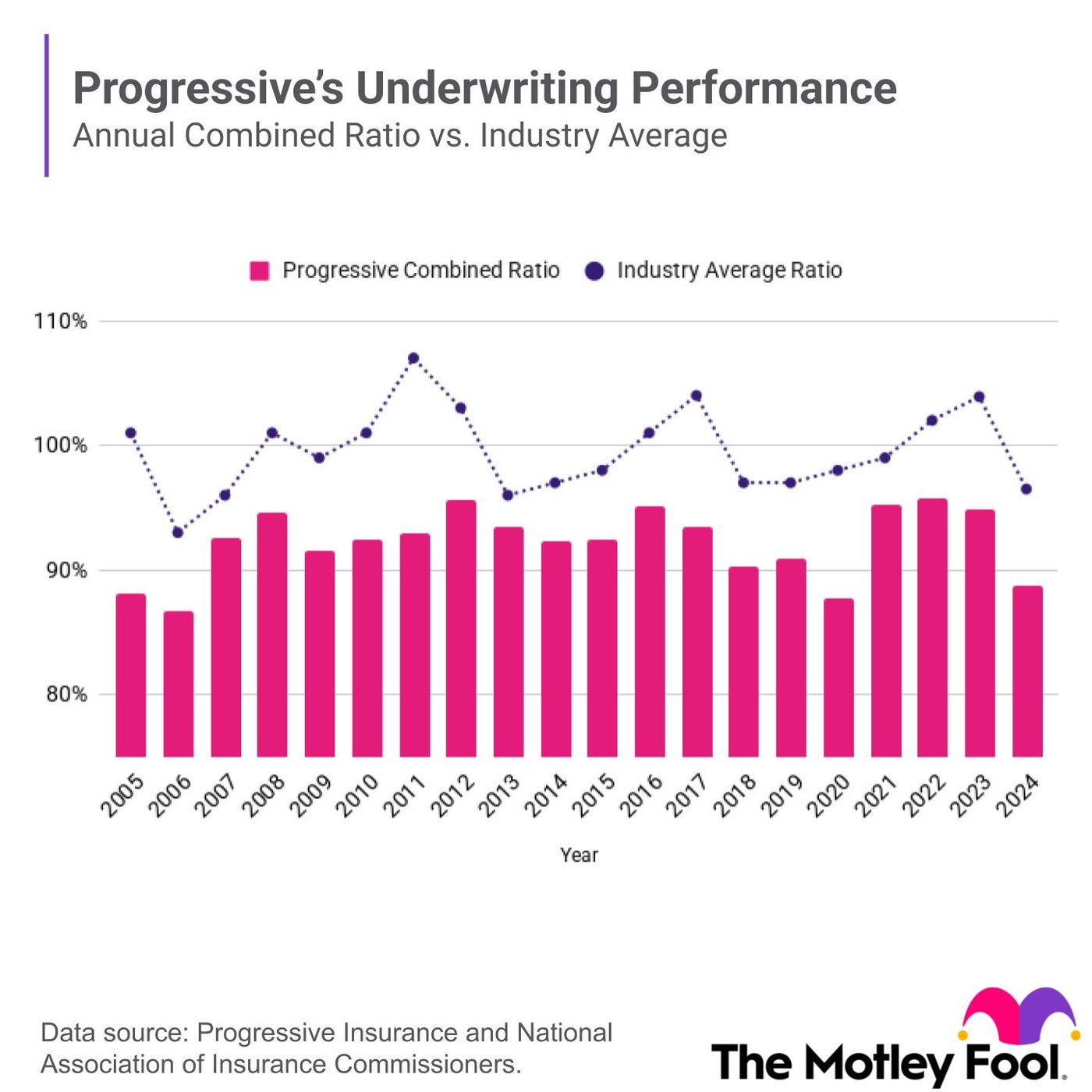

Examining Regency’s solid performance reveals a remarkable 92% average combined ratio over the last couple of decades, which underscores its profitability. While the industry typically hovers around a breakeven combined ratio of 100% due to fierce competition, Progressive’s ability to turn $100 in premiums into an $8 underwriting profit speaks volumes about its operational efficiency.

The Impact of Recent Results on Stock Performance

Recently, however, the company’s stock experienced turbulence following the announcement regarding its financial results for September. Progressive disclosed plans to return approximately $1 billion to policyholders in Florida, a move resulting from prior tort reforms that slashed litigation costs and bolstered underwriting margins. While this refund is a goodwill gesture benefitting around 2.7 million active policyholders, it has temporarily afflicted the company’s underwriting profits, leading to concerns among investors as the combined ratio for September nudged up to 100%.

Nevertheless, let’s not overlook the bigger picture. For the first three quarters of this year, Progressive still showcased an extraordinary combined ratio of 87.3%. Investors are currently anxious over a seeming shift toward a softer pricing environment—a cyclical aspect of the insurance industry. Unlike other cyclical stocks, which are deeply intertwined with the broader economy, insurance companies like Progressive navigate through phases of hard and soft markets. Even with present concerns, should inflation —a potential threat—re-emerge, Progressive can deftly adjust pricing to ensure profitability.

Seize the Opportunity: Progressive is a Buy

As a long-term investor, there’s little cause for alarm regarding Progressive’s short-term struggles. The company continuously demonstrates impeccable underwriting prowess, and any deterioration would reflect in an increased combined ratio—a scenario not currently on the radar. Trading at merely 15 times next year’s anticipated earnings and at its cheapest valuation in nearly two years, this weakness translates to an irresistible buying opportunity.

Considerations Before Investing

For potential investors pondering whether to buy into Progressive, a word of caution: The Motley Fool’s Stock Advisor analysts have recently identified 10 top stocks for investment—but Progressive didn’t make the cut. Historical context shows that those included have yielded extraordinary returns, like Netflix and Nvidia, illustrating the potential for substantial appreciation in the right market circumstances. For those looking for investment success, this could serve as a captivating moment to delve deeper into Progressive while simultaneously exploring other intriguing opportunities.

In conclusion, amid a surging market plagued with valuation concerns, Progressive stands out as a beacon of potential in the insurance sector—a compelling bargain that savvy investors would be foolish to overlook.

Source: finance.yahoo.com/news/why-progressive-stock-incredible-bargain-123000118.html

{kind=link}