The Illusion of Stability in Airbnb’s Business Model

Airbnb, the face of the short-term rental revolution, is struggling to navigate a landscape littered with regulatory landmines and financial uncertainty. Despite its image as a go-to platform for travelers seeking unique accommodations, the reality is a precarious balancing act of appeasing both local governments and users alike.

Regulatory Nightmares

In major tourist hotspots like Hawaii, New York City, and Paris, local authorities wield the hammer of stringent regulations against Airbnb’s operations. Homeowners associations across the country are tightening the noose with restrictive covenants aimed at thwarting property owners who wish to throw their hats into the short-term rental ring. It’s a battleground where compliance and profitability often clash, yet Airbnb persists in championing its business model.

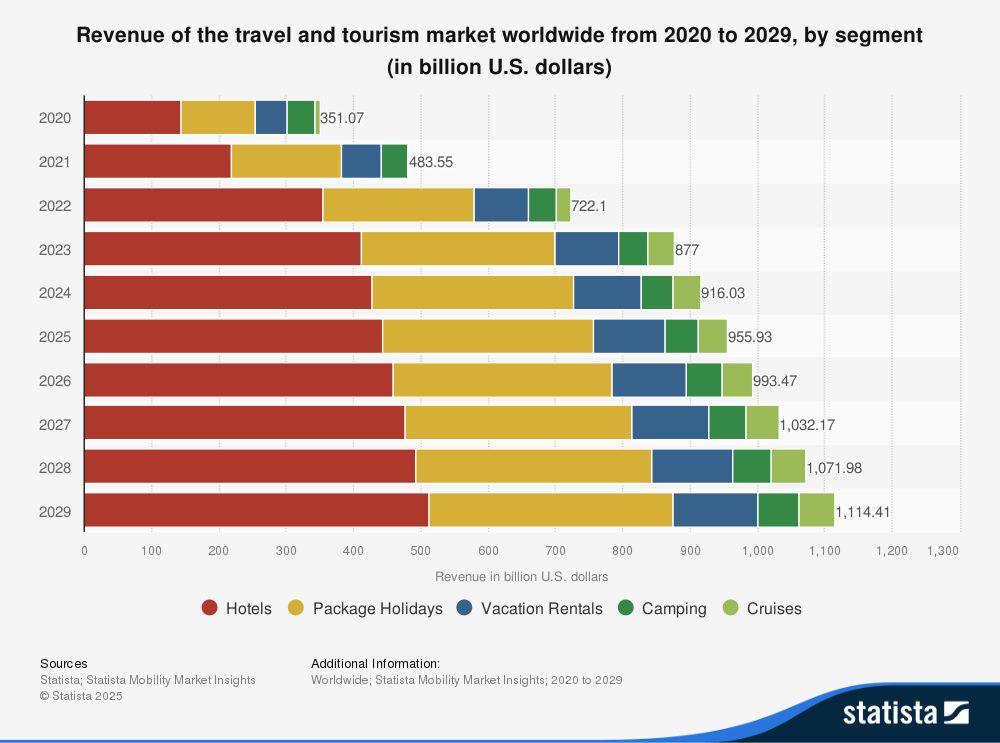

The Market’s Unfathomable Depths

Despite turbulence, the market realm in which Airbnb operates is nothing short of vast. The travel and tourism sector is projected to eclipse $1.1 trillion by 2029, revealing a tapestry of demographic shifts favoring younger generations who have an increasing propensity to choose Airbnb over traditional lodging options.

A Cash Cow? More Like a Cash Muncher

At its core, Airbnb is deceptively simple: a software platform with a customer service facet. Unlike most industries that are burdened by hefty capital expenditures, Airbnb boasts a model characterized by minimal infrastructure investment. While competitors like Intel are entrenched in spiraling capex costs, Airbnb has effectively minimized this drain. This operational style leads to a staggering free cash flow margin of 40%, an enviable figure that presents a facade of financial robustness.

Shareholder Value Amidst Growth Initiatives

Airbnb flaunts its cash flow by funneling it into aggressive growth strategies and stock buybacks, all while inflating the value of remaining shares in a grisly, capitalist feast. By reducing the number of shares available, it deceptively enhances perceived shareholder wealth as if each slice of pizza grows larger in an ever-depleting pie. $3.5 billion dedicated to repurchasing stock in the past year reinforces its financial maneuvering, even as doubts linger.

Valuation Playing Tricks

The question becomes whether Airbnb is genuinely a wise investment choice. Trading at 20 times its free cash flow, it appears to be a discounts sanctuary compared to rival Booking Holdings, which holds a higher valuation. Yet, investors are cautioned to consider the broader implications of such metrics beyond surface-level allure.

A Dissonance of Recommendations

For all these apparent advantages, analysts are suggesting there are ten stocks more compelling than Airbnb, dismissing its appeal outright. These recommendations underscore a deep-rooted skepticism regarding the sustainability of Airbnb’s business model, even as it continues to chip away at the market’s edges.

In Conclusion: A Landscape of Uncertainty

Amidst a backdrop of regulatory strife and precarious financial footing, the façade of Airbnb as a solid investment is beginning to crack. Will its financial engineering triumph in the long run, or is the platform doomed to falter under the weight of its own expectations? The struggle between operational success and regulatory suffocation continues.

Source: The Motley Fool

Source: finance.yahoo.com/news/airbnbs-cash-cow-thrive-despite-130900416.html

{kind=link}