A Titanic Promise of $1 Trillion in Revenue

The computing giant Nvidia stands under the spotlight again, forecasting a monetary colossus in the form of $1 trillion in data center revenue by 2028. With CEO Jensen Huang boasting this inconceivable vision in front of shareholders and industry leaders, the mesmerized audience might miss one critical question: Can this growth be verified by reality, or is it just another seduction of inflated optimism? With no clear competitors reaching Walmart’s stratospheric earnings, can Nvidia truly shatter this ceiling of capitalist imagination?

Over the past year, the data center sector for Nvidia has outpaced market expectations with a staggering 93% year-over-year growth. Yet 93% growth sustained through 2028? If Wall Street had a nose, it would certainly twitch at the scent of this dubious overreach and the potential consequences.

Facing the Giants of Precaution

Let’s rip through the grandeur and dissect the skeleton of challenge. If Nvidia expects a compound annual growth rate of at least 72% over the next four years, anything less spells disaster for its trillion-dollar dreams. Ambition should inspire, but not at the expense of sober foresight—a quality so missing from this hyperglossed projection.

The corporation already faces whispers of uncertainties related to shifts in economic focus and customer loyalties. While Nvidia’s grip on AI hardware dominance remains firm, disruptions caused by increasing competitors or constrained capital budgets could easily distort this flawless profit narrative. The edge Nvidia claims might suddenly dull under competitive markets with divergent technologies rising faster than anticipated.

The Profit Mirage

Here’s the math Nvidia shareholders salivate over: reaching $560 billion in pure profits with a sustained 56% profit margin. Incredible? Yes. Practical? Hardly. Any sane observer knows that growth eventually tapers over time, especially when scaling at breakneck speed.

Profit projections painted against a vapor-thin outline of uninterrupted growth serve one real purpose in Silicon Valley—sustaining insatiable stock speculation. Let’s remember one truth behind those dollar figures: unchecked optimism rarely reflects consistent long-term fundamentals.

If Their Numbers Fail

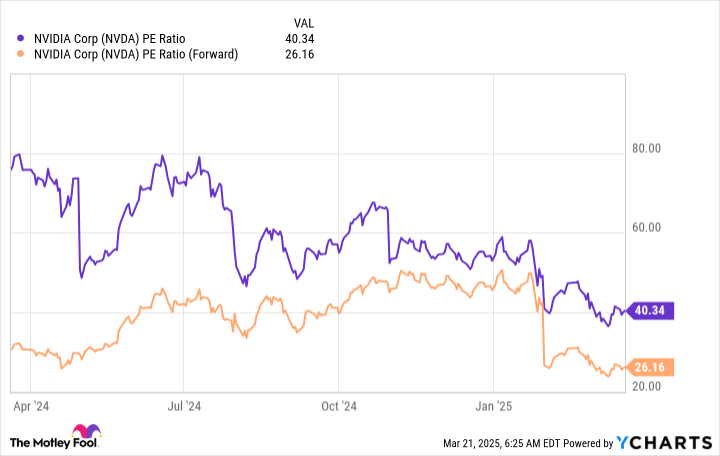

What happens when Nvidia’s utopian figures falter? Sure, devout enthusiasts may argue the company’s stock now trades under more grounded valuations at 26 times future earnings—lower than their flashy tech peers. Truly, it doesn’t rescue Nvidia’s strategic roadmap entirely if the edifice crumbles beneath 72% CAGR expectations falling flat.

Consider the cringeworthy spectacles in financial history of tech darlings punished ruthlessly by Wall Street when overly ambitious objectives vanish into mediocrity. Nvidia risks enduring the same if its quarterly revelations fail the trillion-dollar litmus test.

The Illusion of a Risk-Free Bet

Some cheerleaders rank Nvidia’s gamble as “one worth taking,” despite possibly missing a trillion-dollar summit. Yet we might as well ask this—when did gambling mega-market valuations based on overpromised consumption expectations become acceptable benchmarks within financial integrity? The current scene screams danger wrapped as opportunity.

If the card house collapses, the double-edged sword of modern image management may only amplify Nvidia’s downward market narrative. Profit obsession blinded major players before, fostering cascading instability. Nvidia’s situation will be no different unless rooted conclusions outweigh the sales-pitch sedation Huang perhaps irresponsibly delivered.

Tomorrow: A Titan or a Mirage?

Nvidia appears to march toward legendary status, its ambitions setting it apart as either techno-capitalism’s enduring talisman—or spectacular implosion story. Those banking on $1 trillion might ask themselves whether their bets fund futures solid as steel or empty echoes of shareholder rhetoric. Reality, as it unfolds, will hold those answers.

Source: finance.yahoo.com/news/1-trillion-reasons-why-nvidia-101500253.html

{kind=link}