The Trade Desk’s Crumbling Glory

Watch the giants fall: The Trade Desk (NASDAQ: TTD), once a dazzling star in the adtech universe, is now plummeting back to Earth. Barely holding its head high with the semblance of leadership in connected TV adtech, this company just wrapped up Q4 2024 with a resounding thud. Revenue? An underwhelming $741 million — way below the lofty promises spun by management and analysts alike. This isn’t just a stumble; it’s a spectacular pratfall in a supposedly untouchable sector.

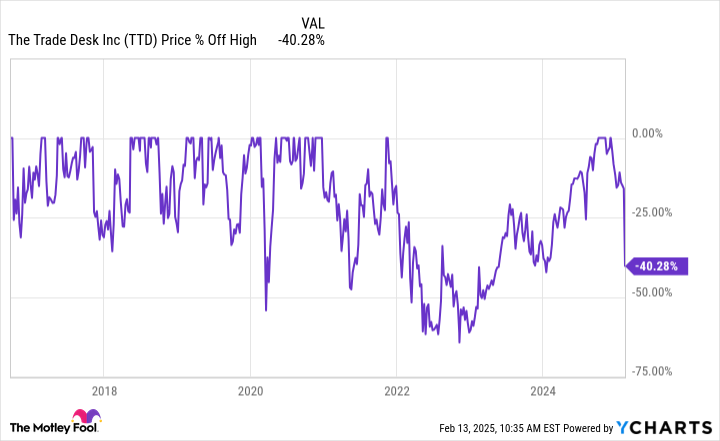

Founder and CEO Jeff Green’s desperate attempt to paint a rosy picture with talk of “successes” could barely hide the glaring admission of failure: “Disappointed that we fell short of our own expectations.” Oh, you think? Investors were left clutching their shattered pride, as the stock nosedived an apocalyptic 31% before 10 a.m. ET. A once mighty TTD is now sitting perilously 40% below its 52-week high. The sweet allure of explosive growth may be fading, and fast.

Deceleration Like Never Before

Let’s not mince words: The Trade Desk is slowing down. In Q4, it boasted a modest 22% year-over-year revenue bump, only to follow it with cringe-worthy forward guidance. The so-called “forecast” for Q1 2025 pegs revenue at “at least” $575 million, reflecting an anemic 17% growth compared to Q1 last year. If that’s the best they can offer, it’s no wonder their investor base is teetering on the edge of an existential crisis.

To add insult to injury, this stagnation isn’t creeping in—it’s steamrolling over any semblance of consistency. Leadership position in adtech? Diminishing returns are proving yet again that market dominion today means nothing tomorrow. Growth investors aren’t merely concerned; they’re probably breaking into a cold sweat.

A Glance at the Shattered Pedestal

Unpopular opinion: A 40% descent from its highs doesn’t mean The Trade Desk is “cheap” now—it’s still ridiculously overpriced, trading at a staggering 17 times sales. Of course, you’ll hear apologists bleating about its market opportunity exceeding $900 billion. Sounds dreamy, doesn’t it? Wake up. Slowly wilted sales growth amid robust aspirations is hardly a formula for prolonged success.

The company likes to point to its 10-year meteoric rise—over 2,600% growth—but conveniently omits the volatility lurking in the shadows. Drops of 40% are barely unusual for TTD; they’re practically its modus operandi. Even if its future holds promise, does it justify the punch-drunk optimism still gripping some observers? Doubtful at best.

Enter the Theatre of Uncertainty

While some still cling to familiar cheerleading about the company’s “resilience,” any rational observer should be questioning the reality of the situation. A leadership role in a $900-billion market sure sounds like a goldmine—until cracks begin to show in execution. Nobody likes to address the elephant waltzing across the ballroom: consistent deceleration, coupled with exorbitant valuations, spells disaster for anyone not already entrenched in TTD’s stock comedy.

Here’s the reality check: The Trade Desk isn’t immune to turbulence. Its price rollercoaster shows a chronic knack for volatility, and this latest debacle is a brutal reminder of just how precarious the growth-stock obsession can be. Forget domination; start bracing for survival.

For the Few Left Standing

Final thoughts? If The Trade Desk thinks it can cling to its past as a bulwark against the future, it’s in for a rude awakening. Stellar market opportunity and obvious sector potential fail to compensate for sluggish growth trajectories. This isn’t just some routine dip—it’s a symptom of deeper issues, bubbling under the surface of an industry infatuated with grandiose prospects but starved of practical reality.

Source: finance.yahoo.com/news/why-trade-desk-stock-got-163630354.html

{kind=link}