Overreliance on Major Banks Fuels Concerns in US Options Market

The US options market is approaching six consecutive years of record transaction volumes, yet a shadow looms over the sector—an alarming dependence on a small cadre of financial institutions to underwrite trades for prominent market makers. As volumes soar, worries about this concentration risk escalate.

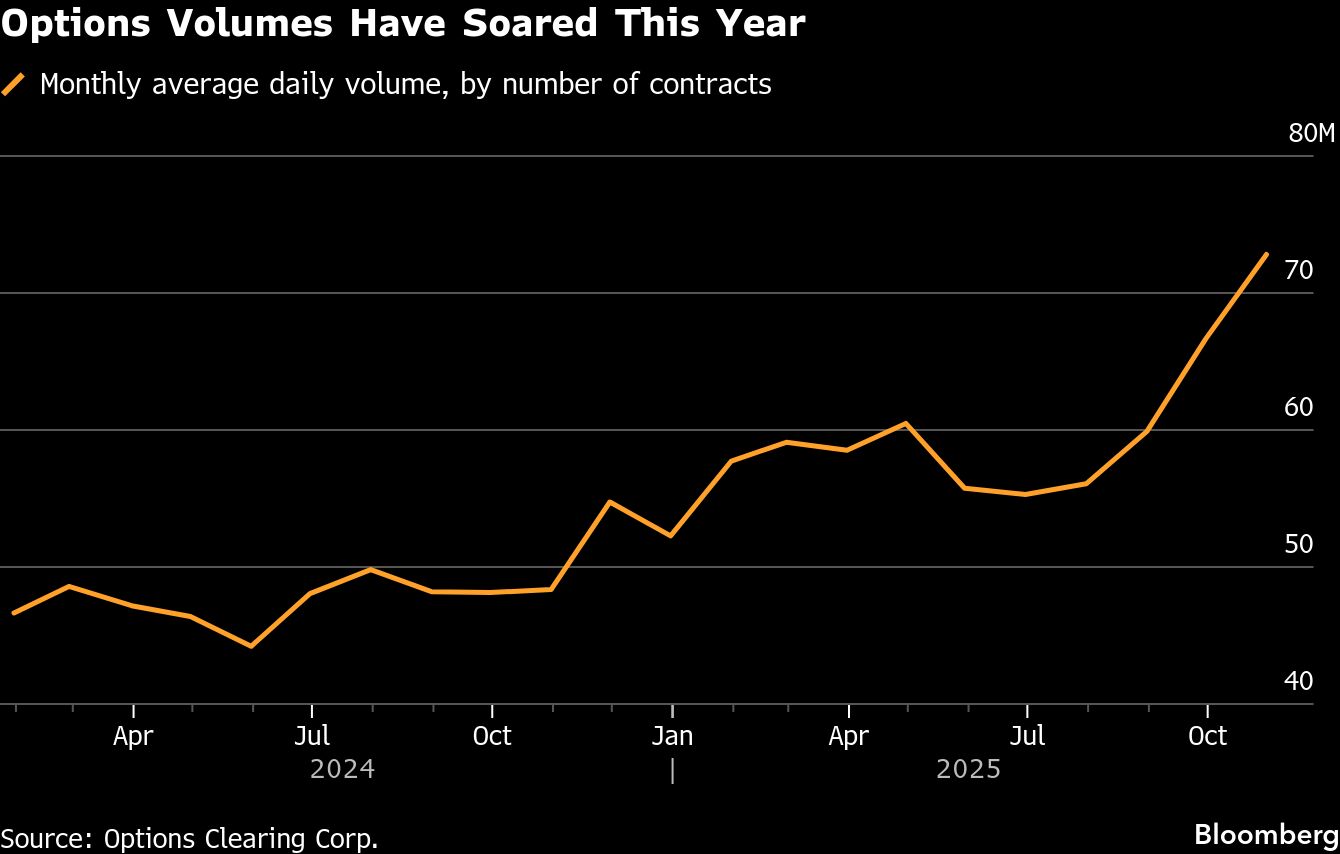

All listed options trades in the US pass through The Options Clearing Corporation (OCC), which serves as a central counterparty processing upward of 70 million contracts daily during peak periods. Members of the OCC act as intermediaries, submitting trades for clearing and providing a safety net should a trading partner falter financially.

The Dominance of a Few Key Players

A mere handful of firms exert substantial control. Of the many members engaged with the OCC, just five are responsible for nearly half of the default fund in the second quarter of 2025. Industry insiders identify Bank of America Corp., Goldman Sachs Group, Inc., and ABN Amro Bank NV as the leading firms managing most industry positions—dangerously funneling most of the market’s activity through these institutions. The repercussions of a failure among any of these entities could be catastrophic.

“There exists an alarming concentration risk in clearing intermediation,” stated Craig Donohue, CEO of Cboe Global Markets, reflecting concerns without explicitly naming involved banks. His insights are tinged with experience—issues of this nature are not entirely speculative; they resonate with a past incident where a clearing member’s bankruptcy had severe implications for the sector.

Capacity Concerns in a Booming Market

While the odds of a major banking failure remain low, the sheer growth of the listed derivatives market presents immediate challenges. The OCC witnessed a staggering 52% increase in average daily volume in October compared to the previous year. This eager surge has prompted market makers to increasingly pursue “self-clearing,” entailing direct membership into the clearinghouse—a precarious move as market makers typically possess thinner capital compared to banks.

Bank of America and Goldman Sachs refrained from commenting on these developments, while ABN Amro remained silent when solicited for a statement.

The Complexity of Cross-Margining

A considerable obstacle also lies embedded within cross-margining—only a limited number of clearing brokers can facilitate it between futures and options. This method allows traders to offset opposite positions in related instruments, ultimately minimizing margin requirements. However, the existing financial architecture entails complexities, with banks often treating cross-margin trades separately, compelling them to hold additional funds against potential risks.

Regulatory Fragmentation Impedes Progress

The fragmented regulatory landscape in the US compounds these challenges. Banks are primarily regulated under the Federal Reserve System, broker-dealers fall under the SEC, and futures remain under the Commodity Futures Trading Commission’s domain. This mishmash creates scenarios where a bank might extend a cross-margining concession while still being mandated to reserve backing funds for trades, complicating financial maneuverability.

Future of Options Trading and Clearing Risks

Emerging trends, such as zero-day-to-expiry options and an uptick in retail trading, introduce fresh hurdles for clearing members. The prospect of 24/7 trading raises alarms about system pressures and necessitates significant investments in capacity and technology. Banks are likely to shift these expenses onto clients; Bank of America has already increased its options-clearing fees, raising charges per trade significantly.

Revising the Default Fund Calculation

In efforts to modernize the risk management framework, the OCC proposes re-evaluating how contributions to its $20 billion default fund are determined. Presently, allocations are influenced by how well a member can withstand roughly 5% market shifts. The OCC seeks approval from the SEC to alter this metric to factor in extreme market conditions, potentially akin to the 1987 crash, where precipitous drops wreaked havoc on the financial landscape.

A Call for Greater Competition in Clearing

Despite risks, Donohue emphasizes the resilience of the clearing houses and the evolving regulatory environment that has adapted to address these threats. He advocates for increased participation in options clearing to enhance competition. “Having more entities with distributed and varied capabilities in clearing would undoubtedly benefit the marketplace,” he concluded, signaling a necessity for diversity in an increasingly concentrated sector.

In sum, as the market hums with unprecedented activity, the looming specter of concentration risk demands attention and action from stakeholders across the board.

Source: finance.yahoo.com/news/us-options-market-grapples-concentration-140000509.html

{kind=link}